One of the most dreaded consequences of the massive, open-ended QE that has been unleashed by the Fed is that of unbridled inflation.

Analysts fear that a result of the huge money printing exercise by the FED could be an overflow of the extra money into the main economy resulting in price increases all around which would negate the inflation targets currently visualised by the FED.

Yet a question arises about the fate of the QE measures taken after the 2008 crisis. How come inflation is still tame around 2% considering the monetary stimulus actions already taken by the FED?

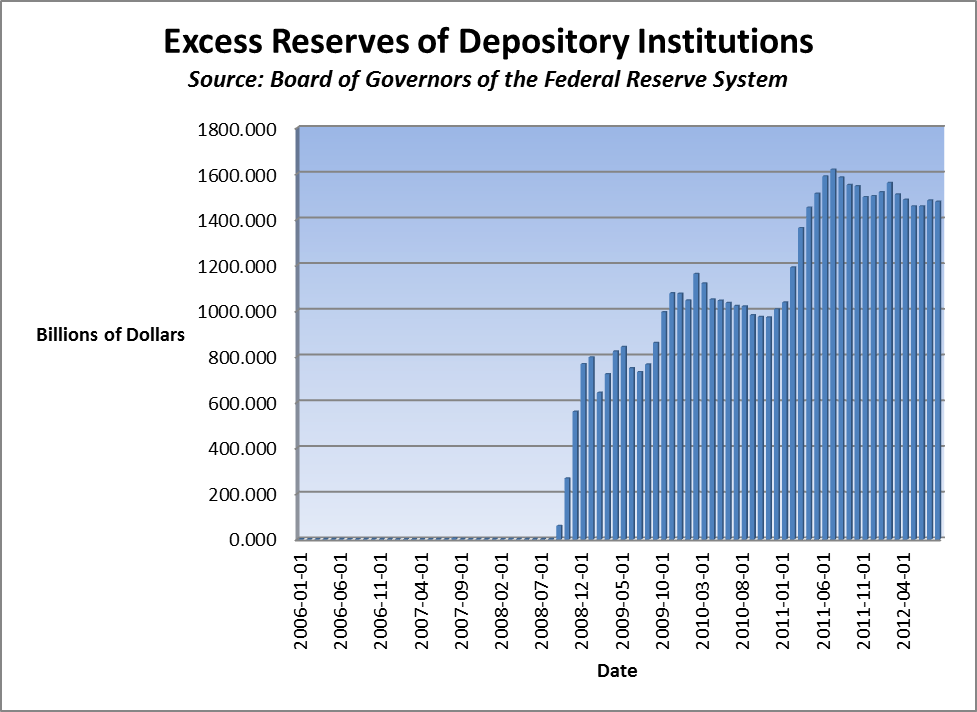

The answer appears to be that most of the stimulus found its way into what is known as “excess reserves with the FED” as shown by the chart below:

As of 1 August 2012, these excess reserves totalled $ 1.48 trillion. Obviously, these funds did not push up inflation because banks preferred to hold them as reserves with the FED rather than lend them out into the economy. Actually, these institutions receive Interest on Excess Reserves (IOER) on these funds from the Fed.

But this figure could pale into comparison with what could be seen around in the middle of 2015 when you add in $ 1.3 trillion account QE3 and another $ 1.5 trillion if Operation Twist gets extended.

In fact, the cacophony of inflation-fearers is now joined by a rising swell of opinions by analysts who in fact claim that the hidden agenda in the FedSpeak regarding QE3 is to actually stoke inflation.

PIMCO’s Dr Mohamed El-Erian is of the view that the United States may now be entering an era when controlling inflation will take a lower priority compared to other objectives such as stimulating growth or employment. He coins the rather expressive catchphrase “reverse Volcker moment” to signify this shift from the years when Paul Volcker determined that crushing inflation was the single most important prerogative of the Fed. El-Erian goes on to state that an average American may now have to contend with inflation “if the Fed is indeed in the midst of engineering a reverse Volcker moment.”

In an interview later with CNBC, El-Erian unambiguously said, “not only will they tolerate higher inflation, not only do they wish for higher inflation, but they actually may target higher inflation.”

Paul Krugman, in his post “The Trouble With Fedspeak,” points to the huge spike in the Tips spread post the announcement of QE3 and said that inflation expectation was the main purpose of the exercise. He says, “inflation expectations are the main target, and a rise in those expectations is a feature, not a bug.”

That may make sense, considering that a huge amount of household wealth was destroyed by the housing bust, and affected consumers are now in a savings mode so as to rebuild their balance sheets. It is not surprising therefore that consumer spending is on a tight leash, and is therefore affecting the economy because it accounts for 70% of the nation’s GDP.

In such a situation monetary inducements such as low interest rates will not have the desired effect. It is likely the Fed may have thought that one way to remedy this situation would be to create an environment where consumers perceive that it is smarter to buy now rather than later in view of rising inflation and the declining purchasing power of the dollar.

The Fed’s preference for inflation is also borne out by its intention to keep in place a “highly accommodative” stance in monetary policy for some time even after the recovery has strengthened, as also to keep the federal funds rate at exceptionally low levels through mid-2015.

Charles I. Plosser, President and Chief Executive Officer, Federal Reserve Bank of Philadelphia, said on September 25, 2012, “and since the Fed said it expects to keep substantial accommodation in place even after the recovery strengthens, people and businesses should be reassured that the recovery will remain intact, even in the face of future adverse shocks. This should make households and firms comfortable spending more today rather than saving, which should, in turn, spur hiring.”

This inflation strategy by the Fed is also detailed by Dr Robert Murphy in a video titled “Inflation is the Plan” which may be seen here.

Leave a Comment