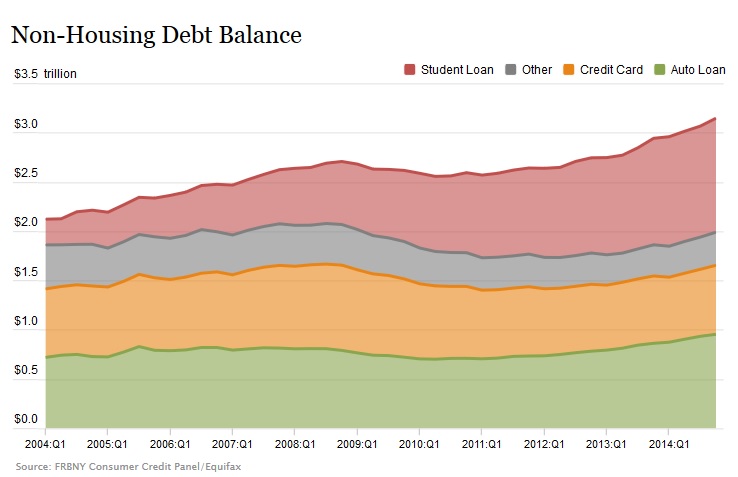

The student loan bubble is on the cusp of bursting. Student loan debt is currently the biggest consumer debt item in the United States today as it has surpassed the $1 trillion threshold.

Although automobile loans and credit card debt are ascending again, even years after the Great Recession that left millions of U.S. households financially paralyzed, the one figure that is concerning many analysts is the $1.16 trillion student debt level, a number that rose by $31 billion in the fourth quarter of 2014.

The only other type of debt that is higher than student loan debt is mortgage debt, which presently stands at $8.17 trillion and rose by $39 billion in the final three months of last year.

On top of this student loan debt statistic, graduates are having a difficult time paying it off.

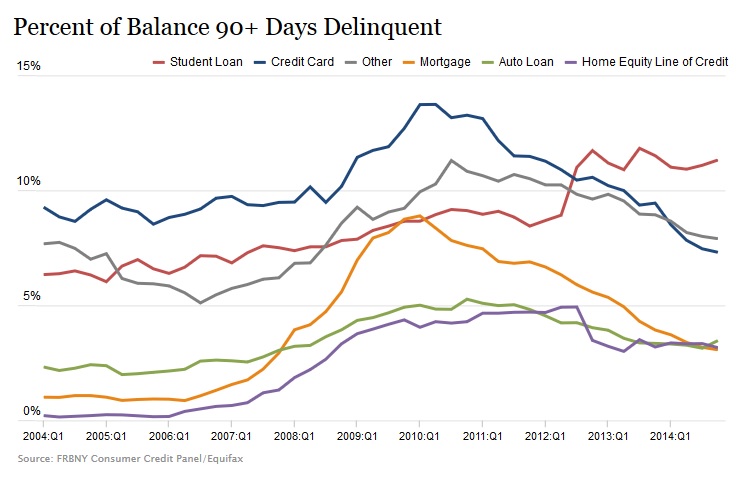

A new report from the Federal Reserve Bank of New York (FRBNY) suggests that the delinquency rate – a loan that is past due by 90 days or more – for student loans stands at 11.3 percent, which is also the highest delinquency rate for all forms of debt. As the delinquency rate falls for credit cards and other consumer debt types, the student debt criteria continues to climb dramatically.

“Although we’ve seen an overall improvement in delinquency rates since the Great Recession, the increasing trend in student loan balances and delinquencies is concerning,” said Donghoon Lee, research officer at the Federal Reserve Bank of New York, in the report. “Student loan delinquencies and repayment problems appear to be reducing borrowers’ ability to form their own households.”

In the last decade alone, student loan debt has skyrocketed from around $260 billion to more than $1 trillion. When compared to credit card debt over the last 10 years, it’s rather minuscule; credit card debt has only gone up from $690 billion in 2004 to $700 billion in 2014.

What is interesting is the fact that Lee has previously warned about the dangers of student loan debt and their delinquency rates. As we reported in 2013, he wrote: “Student loan debt is the only kind of household debt that continued to rise during the Great Recession and has now the second-largest balance after mortgage debt.”

Experts are also warning that millennials are at deep financial risk because they can’t accumulate assets nor can they purchase a house. This exponential debt is placing graduates behind the eight ball, and with an erratic labor market it seems very difficult for them to get out in front.

Leave a Comment