If there is one thing that has happened in the global economy since the financial collapse it’s that more people are indebted than ever before. A new study suggest that there is one age demographic that is facing unprecedented amounts of debt: seniors.

According to a new study by the New York Federal Reserve, Americans in their 50s, 60s and 70s are more in debt than at any other time in history. This is due to an array of factors: aging Baby Boomers facing mortgages, auto loans and student debt.

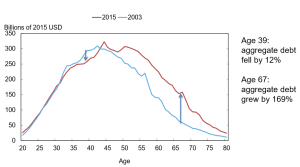

Data from the New York Fed released Friday suggest the average 65-year-old borrowers has 47 percent more mortgage debt and 29 percent more auto debt than 65-year-olds had in 2003.

It should be noted, however, that older borrowers are facing lower default rates and have higher credit scores with greater assets. Delinquency rates for mortgage debt is at 2.2 percent, while credit card delinquencies have been falling.

But an increase in borrowing in the same age group is concerning many.

“The reallocation of debt from young [people], with historically weak repayment, to retirement- aged consumers, with historically strong repayment,” the report said. “Retirement-aged consumers’ repayment has shown little sign of developing weakness as their balances have grown.”

Some may argue the point that seniors are more in debt because they believe the economy is getting better and they think their future is bright. Unfortunately, it’s quite the opposite: they’re having a difficult time in the current economy.

John Rubino of Dollar Collapse opines:

“Older people are carrying more debt not because they’re optimistic about the future but because they’re struggling in the present. Their mortgages aren’t paid off because they’ve used all their free cash on health care and their kids’ upkeep and education. One of the notable features of recent (supposedly strong) US employment reports is the large number of new jobs going to workers 55 and older. The implication is that people who in better times might be retiring are now taking whatever work they can get to make ends meet.”

Consumer debt remains to be an immense issue for millions of Americans. The average household has nearly $13,000 in debt, according to Nerd Wallet. Americans have $712 billion in credit card debt, $8.12 trillion in mortgage debt, $1.21 trillion in student loans and $1.03 trillion in auto loans.

The worst thing about the exorbitant amount of debt consumers have is the interest. The average household pays close to $7,000 a year in interest. This accounts to about nine percent of the average household income.

Leave a Comment