If retail clients were to receive negative interest rates, would there be massive bank runs? That’s what one bank economist thinks would happen.

Speaking at a media conference in Zurich on Tuesday, UBS’s chief economist for Switzerland Daniel Kalt warned that Swiss banks would experience mass withdrawals by deposits if they were given subzero rates.

Right now, the Swiss National Bank (SNB) has imposed a 0.75 percent charge on deposits that are above a certain threshold. This is part of the central bank’s efforts to weaken demand for the Swiss franc. Because of this policy, many of the banks are seeking out ways to deal with the cost of negative rates in order to avoid impacting its day-to-day customers – the financial institutions doled out $1.2 billion to the SNB to park their money in 205. Some reports suggest that they’re thinking of passing them on to the average customer.

Kalt thinks this would trigger a bank run.

“Cash, as banks offer it, is a subsidised asset because we do not pass on negative interest rates,” Kalt said. “Therefore for banks, cash is a certain problem. With each million in cash we get, it’s a loss-making business for us.”

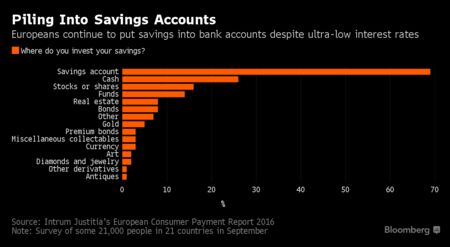

His remarks coincide with a new study that found negative rates are not stopping European consumers from depositing their savings to banks.

Intrum Justitia AB, Europe’s biggest debt collector, discovered that subzero interest rates are failing to lower the savings rates across Europe, which means that the European Central Bank (ECB)’s plan isn’t working. According to the report, 69 percent of Europeans, on average, park their savings in bank accounts.

“After the financial crisis, people have felt a need — even if they have small means — to create some kind of security,” CEO Mikael Ericson told Bloomberg News. “It can’t be that people save in a bank account because of the fantastic returns, so it must be about a sense of security, having money in the bank.”

Here is a chart from the news outlet:

Similar data have been found this year (SEE: Central banks’ negative interest rate policies are already backfiring). Rather than spurring borrowing, negative rates are causing savings rates to go up.

As the Mises Institute wrote, there is no such thing as a negative interest rate. Instead, the only thing that negative rates are are inconvenient charges that can’t be avoided.

It is human nature that no one is willing to give up control of what he possesses now and accept less in the future. Since time preference can never be negative, the interest rate can never be negative. What is called a negative interest rate is merely a deposit charge that is difficult to avoid. Central banks throughout the world are exploiting their ability to charge for reserves held by their bank customers. By calling its charge a negative interest rate, central banks are trying to create the impression that what they are doing is a natural market phenomenon. It is no such thing. Because the central bank has a monopoly on the kind of money that may be used–its own!–and the quantity of money that people and businesses may use within a currency zone, it has the temporary power to force its member bank customers, and by extension its member banks’ own customers, a fee for holding that which they cannot conveniently house anywhere else at the present time. This is nothing more than monetary repression, the purpose of which is to force the banks and their customers to loan, loan, loan, and spend, spend, spend respectively in order to re-inflate moribund economies.

The charade of central banking can come to an end. An important first step for all of us is to stop accepting the central controllers’ corrupt definitions of terms that we use to describe reality. Economics is not an opinion; it is a science of reality. Definitions matter.

Let’s just have the market dictate interest rates and not the supposed smartest people in the room.

As the People become more aware of the lie of the central Banking System, they are finding ways to avoid it.

Precious metals will always be a good substitute, as will alternitive economies, (the Barter System).

Nevver keep more in the bank than you are willing to lose.