United States government debt and budget deficits are projected to explode within the next 30 years, warns a new report from the Congressional Budget Office (CBO).

According to a new report released by the non-partisan budgetary agency, debt to gross domestic product (GDP) is expected to reach 150 percent by the year 2047, if government spending remains unchanged. The CBO also warned about the increasing debt burden that is likely to occur amid rising interest rates by the Federal Reserve.

When it comes to the budget deficit, researchers say it will triple to 9.8 percent in 30 years. Today, the deficit sits at around $600 billion.

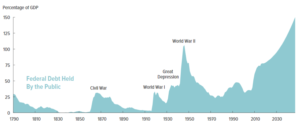

Here is a chart produced by the CBO pertaining to the nation’s history of debt:

Ultimately, the CBO is warning of a heightened chance of a fiscal crisis, one that would impact everything from pension funds to financial institutions. Essentially anyone holding government debt would be negatively affected by the coming financial crisis.

What can the government do to avert a financial collapse? The CBO says it can implement a combination of three policies: restructure the debt, raise inflation above expectations and adopt large tax increases and spending cuts.

Here is what the CBO writes:

“A large and continuously growing federal debt would increase the chance of a fiscal crisis in the United States. Specifically, investors might become less willing to finance federal borrowing unless they were compensated with high returns. If so, interest rates on federal debt would rise abruptly, dramatically increasing the cost of government borrowing. That increase would reduce the market value of outstanding government securities, and investors could lose money. The resulting losses for mutual funds, pension funds, insurance companies, banks, and other holders of government debt might be large enough to cause some financial institutions to fail, creating a fiscal crisis. An additional result would be a higher cost for private-sector borrowing because uncertainty about the government’s responses could reduce confidence in the viability of private-sector enterprises.”

It is interesting that the CBO now warns of a fiscal crisis. During the previous administration, the national debt surged by at least $10 trillion, but the CBO was relatively silent aside from the usual fiscal update. Now that Donald Trump is in office, the CBO brings this up – is the CBO really non-partisan?

The Republicans and Democrats do not really have any plans to rein in the debt and spending. The GOP is looking for more foreign adventures, while the Democrats are obsessed with transgender washrooms.

The U.S. is doomed.

There is always considerable debate as to the future of monetary and fiscal policies. There are even more arguments as to what the impact on economic variables will be from the future of monetary and fiscal policies. Recently, there has also been debate about what the impact on economic variables was from previous monetary and fiscal policies. At Federal Reserve Chair Janet Yellen’s testimony to congress, she was confronted by some Republicans who claimed that the level of GDP growth since 2008 demonstrates that unconventional monetary policy employed by the Federal Reserve was not effective in restoring economic growth to acceptable levels.

There were many things that Janet Yellen could have said in response. She mostly followed the adage that discretion is the better part of valor. She pointed out that the dual mandate from congress to the Federal Reserve is to limit price inflation and unemployment while there is no specific congressional mandate regarding GDP growth. She pointed to the fact that the Federal Reserve targets regarding price inflation and unemployment have been largely achieved. She did also say that GDP growth has been disappointing.

This debate concerning how effective what could be termed “unconventional monetary policy” has been is relevant in terms of what we can expect going forward. An interesting thought experiment can be conducted to determine what would have occurred if unconventional monetary policy not been implemented by the Federal Reserve during the last eight years. We know that unemployment has gone from over 10% to less than 5%. That was accomplished primarily through monetary policy. The same reduction in unemployment could have been accomplished primarily through fiscal policy. However, if that had been done, some things now would be different.

Both monetary and fiscal policies can be used to stimulate the economy and thus reduce the unemployment rate. Stimulative monetary and fiscal policies both work by shifting the aggregate demand curve to the right. This results in an equilibrium where unemployment is lower. There is certainly some amount of additional fiscal stimulus that would have brought unemployment to where it is now, even if there had been much less stimulative monetary policy. Whether from tax cuts or additional government spending, relying primarily on fiscal policy over the past eight years would have resulted in significantly higher deficits and thus levels of Federal debt.

Using mostly fiscal policy rather than monetary policy to promote the recovery from the 2008 economic crisis would have meant that interest rates would have been higher over the last eight years than was actually the case. The higher interest rates would have increased deficits and thus levels of Federal debt separate from the impacts on the deficits that higher spending and/or lower taxes bring. Higher interest rates increase deficits and debt, as interest expense is an important part of government expenditures. See: Long-Term Federal Budget – It Is Worse Than You Think http://seekingalpha.com/article/3998673-long-term-federal-budget-worse-think

The results of the thought experiment are that if fiscal policy rather than primarily monetary policy has been used to cut the unemployment rate in half in the aftermath of the 2008 financial crisis, we would have the same unemployment rate as we do now, but a much greater Federal debt. I believe this suggests that monetary policy is generally a superior policy tool than fiscal policy in terms addressing the consequences of a financial crisis.

In America, we have relied primarily on monetary policy rather than fiscal policy, not as much from a deliberate decision to do so, but more from political gridlock. President Obama pushed for additional fiscal stimulus during most of the period. The Republicans in congress prevented Obama’s additional stimulus plans from being enacted. In most of the other developed countries, especially in Europe, reliance on monetary policy rather than fiscal policy has been more of a deliberate decision. Possibly, the proximity to Greece and the other European countries that experienced problems stemming from excessive government debt influenced the choice to use monetary rather than fiscal policy…”

http://seekingalpha.com/article/4047608