This is going to be truly terrifying when interest rates start to rise exponentially.

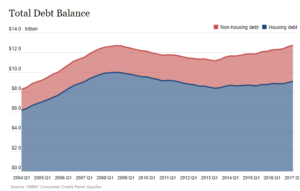

According to new data from the Federal Reserve Bank of New York, total consumer debt – auto loans, credit cards and mortgages – hit $12.7 trillion in the first quarter of 2017. This surpasses the previous peak in 2008, just prior to the economic collapse.

Interestingly enough, America’s total consumer debt is four times the economy of Germany and is about the size of the Chinese economy. Yikes!

Here is a chart from the New York Fed:

We tend to associate immense consumer debt with credit cards – credit card default rates are modest now – but in today’s economy it’s auto loans and student loans. Auto liabilities are sitting at all-time highs, while 11 percent of student loans are either in default or in 90-day delinquency.

Bloomberg reports:

“People are borrowing more not necessarily because they’re confident about their financial prospects. They’re doing it for necessities like education or transportation and, in many cases, just to get by.”

When the tidal wave of price inflation occurs, will they take on even more debt?

50 percent of workers make less than $30,000 per year. Even at the current low interest rates, we are paying more interest on car loans and home loans today, because the amount financed is 5 to 10 times higher than it was in 1970. Real wages have just not kept up with price inflation. No wonder the average family debt has increased. I am surprised it is not higher than the 2008 levels, but I am sure it is for many families.

Well, when you have nothing but false currency instead of a real value currency, the manipulation of the numbers can create this inflation with out impunity; except of course the coming financial crash in toto.