Although the Bank of Canada (BOC) seems to have hit the pause button on raising interest rates, they are still higher than they were a couple of years ago. As a result, consumers are getting hit in the wallet because they borrowed too much and spent more than they earn. So, when rates go even higher, they’ll be in for some pecuniary troubles.

The economy is already beginning to notice insolvencies.

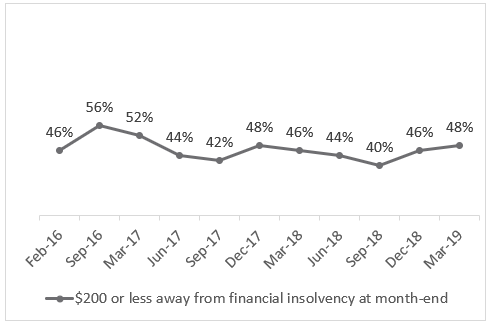

According to the Office of the Superintendent of Bankruptcy (OSB), the number of Canadians who filed for insolvency in the first quarter of 2019 was up six percent compared to the same time a year ago. In the two-month period ending March 31, 127,109 Canadians became insolvent.

Grant Bazian, President of the country’s largest insolvency firm, MNP LTD, says that the numbers may be higher because many households may “sweat it out for years before reckoning with their debt.”

“Based on our research since 2016, we know there are many Canadians experiencing this kind of financial distress. This isn’t good news but it’s something that needs to be discussed so we can eliminate the stigma associated with asking for help and – if it is the best course of action – filing a proposal or bankruptcy,” he says.

“Some of the concern Canadians feel about their debt undoubtedly stems from a lack of financial literacy and awareness about relief options. Canada has a robust, regulated system to help severely indebted individuals regain financial stability.”

Canada is already running on a treadmill, unable to post any meaningful growth. If the consumer is tapped out, then the Canadian economy, which relies heavily on consumer spending, will run on empty.

Leave a Comment