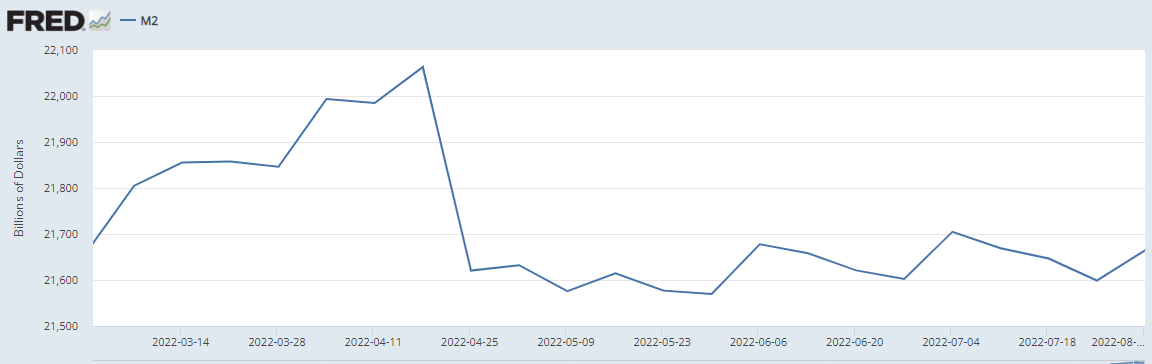

Despite the Federal Reserve raising interest rates and trimming its $8.9 trillion balance sheet, money-supply expansion has yet to fall off a cliff.

Although there was a sharp drop in the M2 in the week beginning April 11, there has been an ebb and flow of the printing presses since the end of April.

Here is what we are seeing based on the St. Louis FRED data:

The U.S. central bank has turned ultra-hawkish, with plans to keep raising interest rates heading into 2023 and leaving them there by the time the world flips the calendar to 2024.

But is this really tightening?

When the fed funds rate is in the range of 2.25 percent and 2.50 percent, and the annual inflation rate is north of eight percent, the real rate (inflation-adjusted) is about negative six percent.

Therefore, it is safe to say that monetary policy is still highly accommodative.

Since it takes about six to nine months of policy updates to seep into the economy, the effects of a rising-rate environment are starting to be felt, whether it is in the form of waning consumer demand or slow business activity.

Of course, investors are hitting the sell button with the financial markets forward-looking. How much they are pricing in a higher-for-longer rate policy remains to be seen.

While the U.S. economy is in a technical recession, the nation might not witness a sharp downturn until next year.

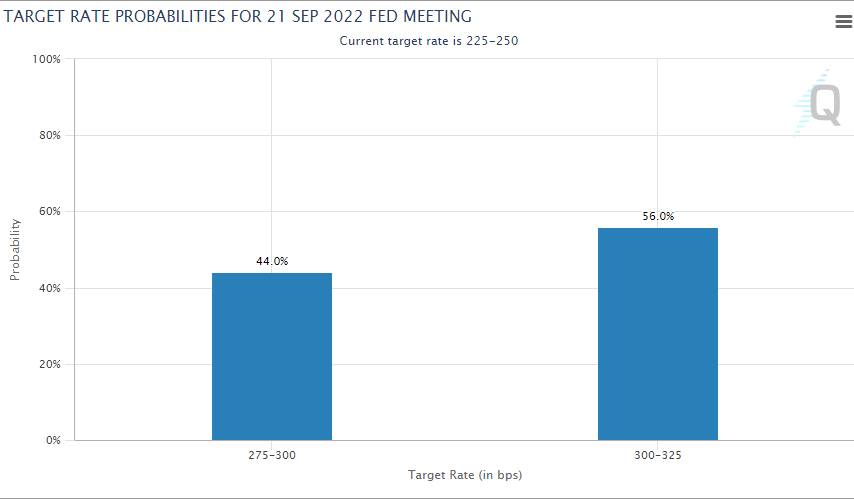

Until then, investors are split as to whether the Eccles Building will pull the trigger on a 50- or 75-basis-point rate hike at the September Federal Open Market Committee (FOMC) policy meeting. But if Fed Chair Jerome Powell and his merry band of central bankers really wanted to restore price stability, it would need to emulate Paul Volcker.

Leave a Comment