Sure, all the focus is on the debt ceiling in Washington.

Both sides will inevitably reach a conclusion and strike a last-minute agreement to raise the debt limit.

Unfortunately, the private sector is also drowning in red ink.

The Federal Reserve Bank of New York (FRBNY) published its latest Household Debt and Credit Report for the first quarter.

What did the central bank researchers find? Total household debt surged by $148 billion, or 0.9 percent, to $17.05 trillion in the January-to-March period.

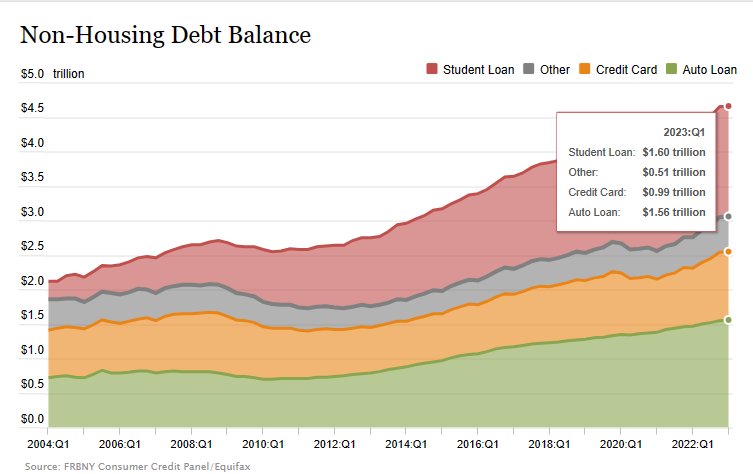

Here is what happened in the first three months of 2023:

- Mortgages: +$121 billion to $12.04 trillion

- Auto Loans: +$10 billion to $1.56 trillion

- Student Loans: +$9 billion to $1.60 trillion

- Others (retail cards and other consumer loans): +$5 billion to $510 billion

- Credit Cards: Unchanged at $1 trillion

“The mortgage refinancing boom is over, but its impact will be seen for decades to come,” said Andrew Haughwout, Director of Household and Public Policy Research at the New York Fed. “As a result of significant equity drawdowns, mortgage borrowers reduced their annual payments by tens of billions of dollars, providing additional funding for spending or paydowns in other debt categories.”

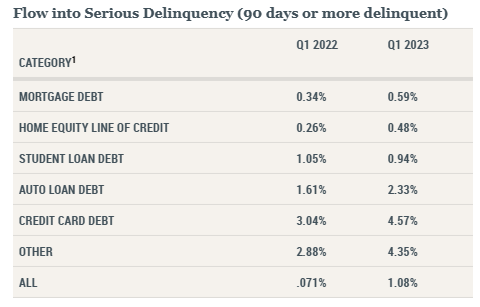

Delinquency rates also soared year-over-year.

Here is a look:

The U.S. is in the middle of a debt crisis and it will not improve anytime soon.

Leave a Comment